- The Weekly Buzz 🐝 by Blossom

- Posts

- 😬 Nvidia Saves the Market?

😬 Nvidia Saves the Market?

A breakdown of Nvidia's blowout earnings report...

Maxwell Nicholson

February 26, 2026

SPECIAL EDITION

✨ Nvidia Saves the Market (Again)

😬 Once a quarter, the market holds its breath as Nvidia ($NVDA) reports earnings…

😰 This quarter in particular, AI jitters have been riding high. Nearly all the major AI players (Microsoft, Google, Amazon) saw big stock drops after earnings, as investors continue to question the massive spending AI spree that seemingly has no end in sight.

🥳 With all this stress, a lot was riding on earnings last night… and Nvidia delivered. The stock initially jumped 4% after earnings, but opened this morning down 3% (but is still in the green over the past week)

🤿 So let’s dive into the report and break down what it means for both Nvidia and the AI boom or bubble (depending on who you ask 😜)

🏆 Nvidia Smashes Revenue & Earnings

📊 First, let’s take a look at the numbers:

💰 Revenue: $68B, up 73% from last year, and 2.9% higher than analysts expected

🎯 Forward Revenue Targets: $78B, ~7% higher than analysts expected

💸 Earnings per Share: $1.62, ~6% higher than analysts expected

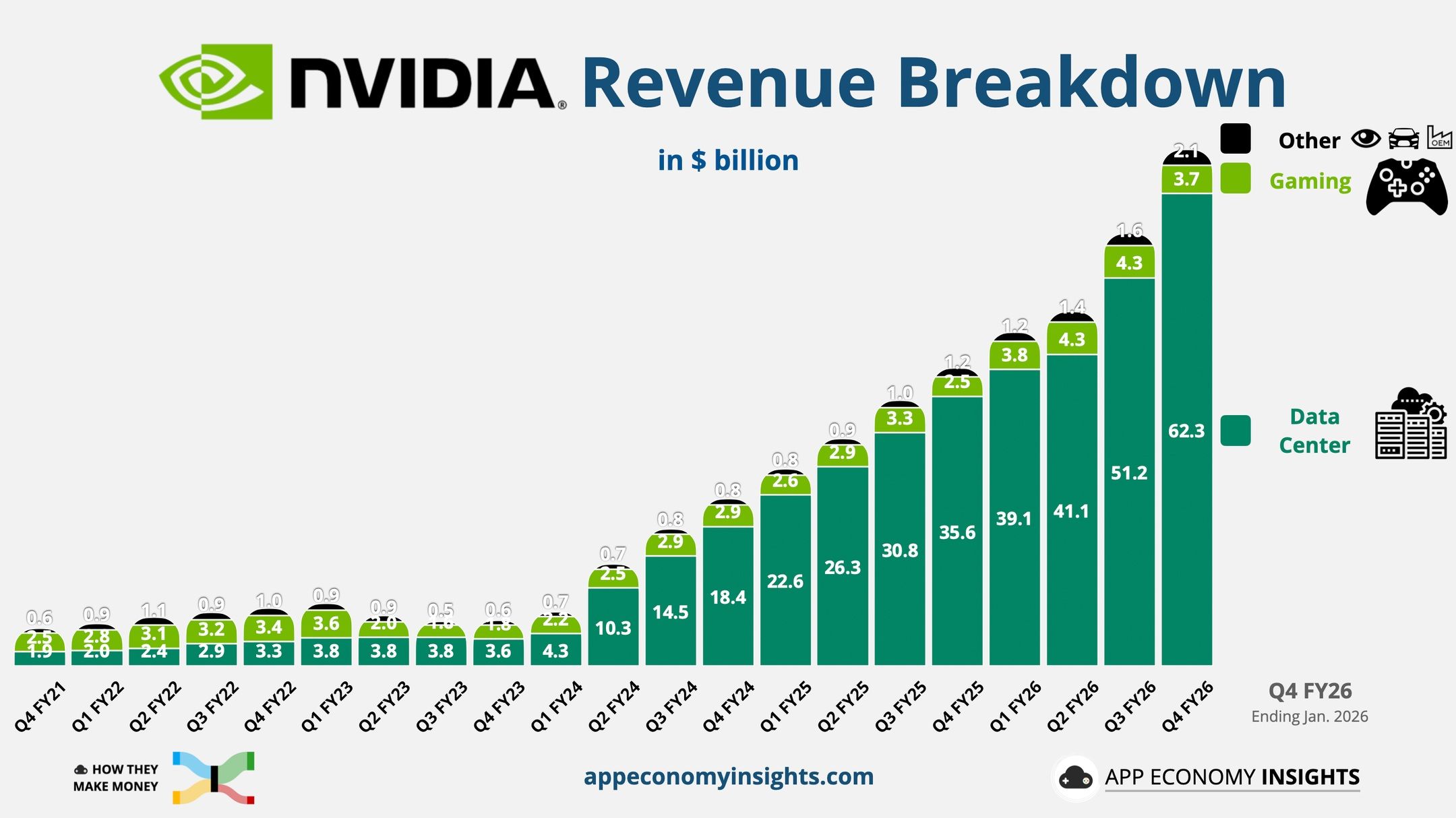

🤯 AI-driven data centre revenue now drives over 90% of Nvidia’s revenue, up from 60% just 3 years ago and just 38% 5 years ago.

🤔 And all this shouldn’t really come as a surprise... while the rest of the Mag 7 saw their stock prices fall after earnings, one thing was consistent: the massive increases in AI spending commitments:

Amazon ($AMZN) announced its AI spending would hit $200B this year (up 60% from last year)

Google ($GOOGL) is planning to spend $185B (double last year)

Microsoft ($MSFT)’s AI spending rose 66% in the most recent quarter to a record $37.5B.

👎 Investors reacted negatively to this as they started to question when this wild spending would show returns, but as long as Mag 7 continues to spend big, Nvidia will continue to rake in the cash.

✨ But outside of the numbers, let’s take a look at the 3 big themes from Nvidia’s earnings:

🚀 1) Revenue Continues to Accelerate

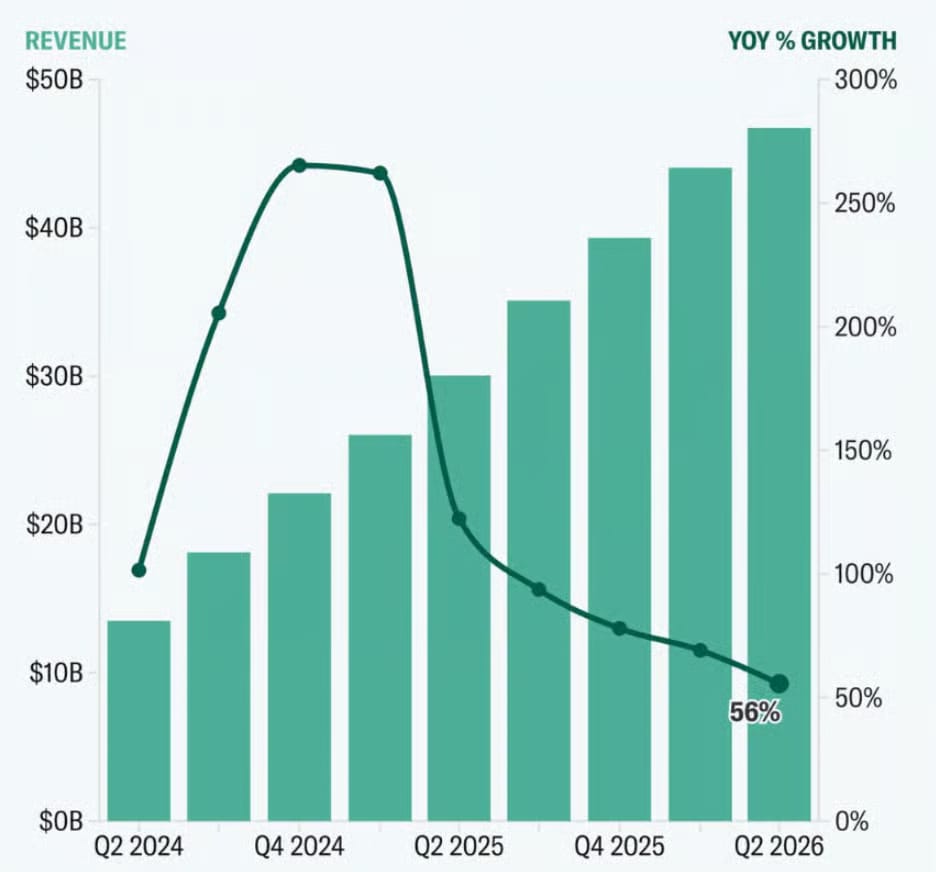

📉 Two quarters back, I shared this chart and talked about how Nvidia has posted revenue % growth declines for 9 straight quarters:

🤯 Well in Q3 (last quarter), they turned this around, with 63% year-over-year growth. This quarter, that uptrend continued with 73% growth. The fact that Nvidia is not just growing, but that growth is accelerating, is truly amazing.

🏆 Leading the charge is Nvidia’s networking business. Nvidia breaks down its data center business into compute (CPUs and GPUs) and networking. This quarter, compute revenue grew a strong 58%, but networking soared 263% to $11 billion (~20% of data center revenues).

🔗 Networking is the high-speed infrastructure that connects thousands of GPUs together so they can operate as a single AI supercomputer. As hyperscalers build massive AI “factories,” Nvidia isn’t just selling the chips, it’s capturing a growing share of the entire data center build-out.

😰 2) Heavy Exposure to Hyperscalers

🐻 The accelerating growth is certainly exciting, but on a more negative or ‘bearish’ note, Nvidia reported that more than half of its revenue comes from the 5 big ‘Hyperscalers’ who almost all plan to double their spending this year (Microsoft, Meta, Amazon, Google, and Oracle).

💰 The problem with this is that it’s unclear how long this can go on. Up until last year, the Hyperscalers were spending less than their quarterly free cash flow, meaning they weren’t having to dip into their cash reserves.

😥 But this year, that’s changing as spending is expected to surpass cash flow, meaning Hyperscalers will have to issue debt and/or dip into cash reserves to cover spending increases.

🃏 This means Nvidia has a LOT riding on these 5 companies and basically needs them to keep up these massive spending increases (and withstand continued investor pushback) to keep up its massive growth.

😎 But Jensen Huang is confident that the other 50% of Nvidia’s customers will also continue to keep the AI spending spree going, pointing to the buzz around new tools like Open Claw as evidence:

“Agentic AI has reached an inflection point, and it literally happened in the last 2 or 3 months. After agentic AI, he added, there will be physical AI, as new AI models are integrated into robotics and manufacturing equipment. “

🇨🇳 3) Still No China Revenue

❌ China was a big pain point for Nvidia in the past, with Trump banning Nvidia from selling H20 chips in the country, costing Nvidia $4.5B two quarters back.

😥 In July, that ban got reversed, but despite government approval for shipments of its H200 chips to China, Nvidia CFO Colette Kress said the company has "yet to generate any revenue" from the country, and she isn't sure if any imports of its chips will be allowed.

⚠️ While this obviously hasn’t slowed Nvidia’s growth, it does pose a major risk. After a string of AI IPOs in China (that we covered here), Nvidia's Chinese competitors are gaining momentum with Nvidia’s CFO saying:

“Nvidia’s Chinese competitors have the potential to disrupt the structure of the global AI industry over the long term. America must engage every developer and be the platform for choice for every commercial business, including those in China.”

⁉️ Now to the questions on everyone’s minds… bubble or boom? Is Nvidia overvalued or undervalued? Before we dive into what analysts have to say, a quick word from this week’s sponsor Global X Canada…

PRESENTED BY GLOBAL X CANADA

⭐️ A Modern Way to Access Growth, Income, and Diversification

⚖️ Built for Changing Markets

Markets continue to evolve. Volatility can persist, income opportunities may be hard to find, and managing multiple investments can add unnecessary complexity.

The Global X Growth Asset Allocation Covered Call ETF (GRCC) is designed as an all-in-one portfolio solution intended to help simplify how investors approach income and diversification.

🌎 A Globally Diversified Foundation

GRCC seeks to invest in a globally diversified portfolio of exchange traded funds with a target allocation of approximately 80% equity and 20% fixed income, providing broad exposure across regions and asset classes within a single ETF.

💵 Income Potential, Systematically Applied

In addition to its asset allocation, GRCC benefits from an actively managed covered call overlay. This option-writing approach is intended to generate option premiums, which is designed to deliver high monthly income.

🎯 One ETF, Streamlined Approach

If you prefer a streamlined all in one portfolio approach with built-in diversification and income potential, GRCC may be worth exploring.

Learn why. Watch the video to learn how combining equities, bonds, and covered calls can help support a more consistent investing experience.

*See Global X Canada Disclaimer at the end of the newsletter

NVIDIA EARNINGS CONT.

🫧 Boom or Bubble? What Are Analysts Saying About Nvidia

💡 First, I’ll start by sharing an interesting chart: Nvidia’s price-earnings ratio, a common measure of whether a stock is under- or overvalued.

⭐️ Currently, Nvidia’s P/E is at ~40x, roughly the same level it was at a year ago and lower than levels from even 2017/2018, long before the AI bubble. For reference, the S&P 500’s PE ratio is 30x, so Nvidia’s multiple isn’t too far off. This suggests that Nvidia’s valuation hasn't run too hot compared to its fundamentals and could even be undervalued.

🎯 Analysts agree, reacting with ‘overwhelming optimism’ to Nvidia’s earnings, with 35/36 analysts covered by TipRanks maintaining buy ratings with an average price target of $267, 37% above the current price.

An analyst from D.A. Davidson summarized the sentiment well:

“We are simply not seeing demand slowing down for compute for the foreseeable future”

Many called out that Nvidia is suffering from AI jitters:

“The lack of a meaningful reaction to Nvidia's earnings report shows how skepticism continues to pervade large-cap AI stocks. Market sentiment is very tepid. The stock is not reflecting Nvidia's fundamental”

⚠️ But that doesn’t mean there aren’t major risks. Nvidia’s success is in direct correlation with the rising AI spending, and the many fears of how long the massive capex can continue to grow are very real.

💡 Even in periods of massive technological progress, infrastructure can get overbuilt. The internet has been no doubt transformational, but in the late 1990s dotcom bubble, companies invested over $1 trillion in fiber-optic infrastructure, much of which went unused.

⁉️ The big unknown is where we are in the AI buildout. Are we still in the beginning, or are we at the ‘overbuilding’ stage? As one analyst put it:

“The real debate is what growth looks like in 2027 and 2028. Ultimately, investors have to decide what inning of the AI buildout we are in”

👀 And ultimately… that’s up to you to decide. If you’re curious what other investors are thinking - join the discussion on Blossom!

👋 Thanks for reading! For those new here, my name is Max (@maxstocks) and I'm the CEO of Blossom and author of the Weekly Buzz 🐝 Drop me a follow on Blossom if you want to see what I’m investing in!

SPONSORED BY RBC DIRECT INVESTING

Invest Now

Start trading on your terms. Get 50 commission-free stock and ETF trades per year with GoSmart new from RBC Direct Investing.

CANADIAN TOP PERFORMERS

🚀 The TSX Venture50 List is Live, Showcasing 50 Stocks With Average +431% Returns

😎 This one’s a repeat from last week, but I thought I’d reinclude it in case you missed it!

🏆 The TSX just released its annual Venture 50 list, a ranking of the 50 top-performing companies on the TSX Venture Exchange over the past year, scored equally on share price appreciation, market cap growth, and trading volume… and some of the numbers were truly eye-dropping…

📊 In 2026, the 50 companies on this list posted an average price performance of 431%, generating over $17 billion in new market cap. To highlight a few:

Santacruz Silver Mining ($SCZ), a Latin America–focused silver producer, ranked #1 with an incredible +1103% share price growth

Ucore Rare Metals ($UCU), a North American critical-minerals company focused on advancing secure rare earth refining, ranked #2 with +627% share price growth

Millennial Potash ($MLP), a development-stage potash company with direct access to fertilizer markets in Brazil, the United States, and Africa, ranked #3 with +950% share price growth.

⛏️ Interestingly, mining accounted for 48 of the top 50 performers, marking what the President of the TSX Venture Exchange describes as a clear inflection point for the market:

“The list showcases a historic year for junior mining and high-tech innovation, reflecting an increase in global investor demand and market confidence in the Canadian capital markets at a time when resource security, critical technologies, and domestic supply chains have become strategic priorities worldwide.”

🌼 Blossom is an official media partner of the TSX Venture 50 this year, so if you want to dig into the full list and add some of these stocks to your watchlist, be sure to check the “Markets” tab on the app (mobile-only) or check out the list here on the TSX website!

Global X Canada Disclaimer

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

For more information on Global X Investments Canada Inc. and its suite of ETFs, visit www.GlobalX.ca

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

© 2026 Global X Investments Canada Inc. All Rights Reserved.